The Single Founder Risk Premium

I’ve spent a reasonable chunk of my life thinking about redundancy. I’m not clear whether this is some kind of loss aversion gene or just an early exposure to gaming live ops but it always lingers in the background.

In the wake of the SpaceX IPO, it seems perfectly natural (to me) to have an ongoing obsession with Carrington and Miyake level solar events as things we just don’t think about enough (it’s always surprising to me how relatively little we understand about the sun). As it now seems clear that a lot of this century’s general capitalism (not to mention people’s retirement accounts) will be focused on space, it’s maybe not a crazy idea to understand the key concepts of things which might lead to investment loss (and/or civilisational annihilation). I spent part of the weekend reading this paper about a concept of using solar weather geo-engineering to create a possible defence against these extremely rare (but definitely non-zero) events. It’s quite readable.

Redundancy also makes me think about single-founder risk. Elon Musk is demonstrably one of the best builders and capitalists our planet has produced but I worry deeply what happens to $SPCX’s stock price if he dies prematurely (it’s a morbid but still useful thought experiment I run with a lot of public companies). Traders want founder-run companies, investors want professional management teams. Transitioning founder-driven companies to non-founder management teams is extremely hard and the biggest tech companies have a mixed record. I’m unclear how Alphabet truly works in this regard (Sergey Brin came back to run AI) but it seems to have mostly worked extremely well with Sundar Pichai. Amazon is performing well under Andy Jassey, as is Microsoft under Satya Nadella. Meta seems to have done this quite well for its acquisitions but Zuck is still very clearly directing everything.

All that being said, if you want a company guided through a major phase transition, it’s hard to beat putting founders back in the hot seat. Intercom’s sale to Salesforce (congrats Eoghan, Des and team) capped a remarkable journey that will become a case-study for pivoting to enterprise AI and there are lessons in here for everyone tackling this challenge.

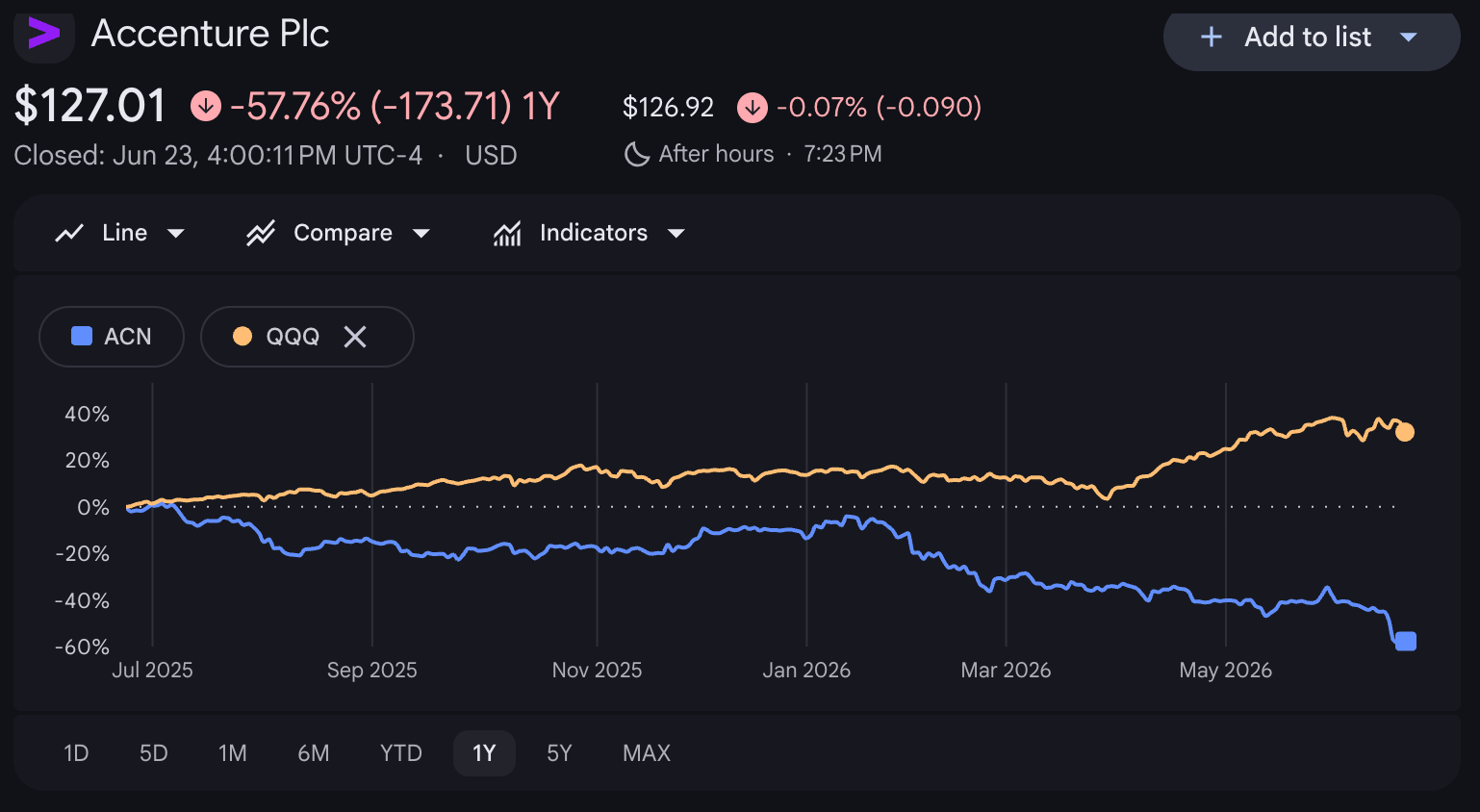

A related curiosity I am mulling is Accenture’s public market performance. At a time when demand for AI consulting and generally applied AI services is basically vertical (which we see through our 10xHumans investments), it is hard to reconcile with a 50% drop in share price. One of these things seems mispriced.

Speaking of founder mythologising, I’ve been working my way through Ada Palmer’s quite good book on the Renaissance and how the period was partially a constructed myth driven by nostalgia for Greek antiquity at the time. It could definitely do with some more robust editing but the individual profiles are excellent and you can gain a lot by just skipping to those.